Brazil Economy Outlook 2019

Brazil has been rediscovered as the darling of emerging markets investors or in other words the shiny letter “B” in BRIC. Whereas China, India, and Russia have been disappointing investors for months all hope is placed on Brazil.

With an outspoken new president and some bombed out markets, Brazil seems to be back on investors’ mind. In the following article, we will look at Brazil’s economic outlook, its potential future under new leadership and the risks investors should rediscover in 2019.

Brazil – The Economy

Jair Bolsonaro, the new president, has been received well by investors. The ‘Tropical Trump’, as foreign media often dubbed him, was inaugurated on New Year’s Day and in the first week of 2019. By then, Brazil was already the best performing stock market in the world.

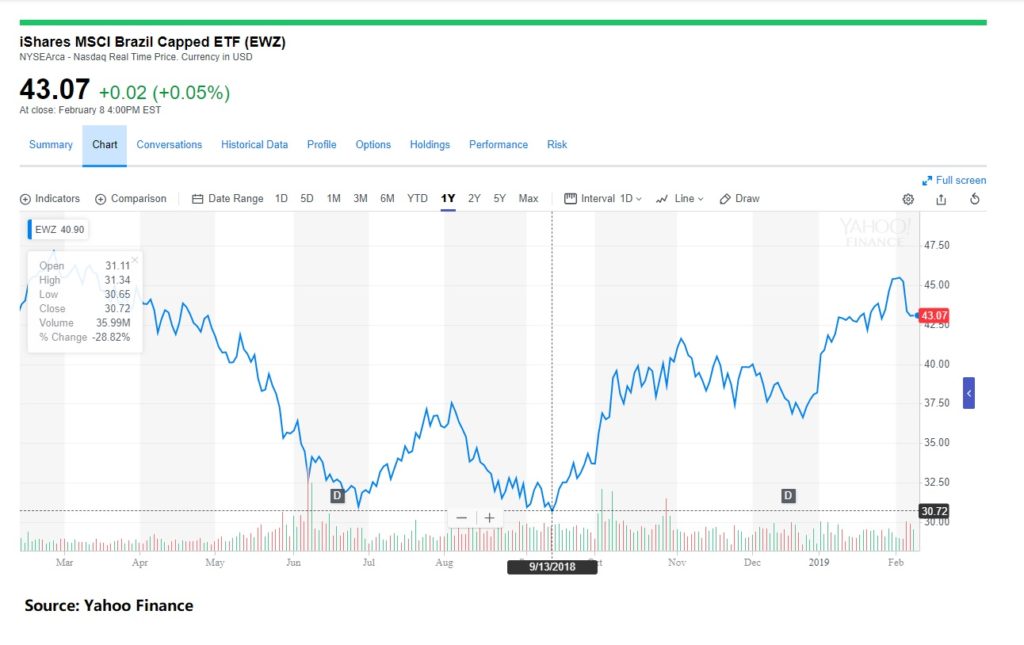

Forbes reports that the iShares MSCI Brazil has been beating the SPDR S&P 500, Russia, India, China, Mexico, FTSE Europe, Japan, and the broader MSCI Emerging Markets Index making it a stock market darling among emerging markets investors and gurus including Marc Mobius who has been very bullish on Brazil for months.

Bolsonaro’s appointments of capable people into key positions and his decision to merge certain ministries have been welcomed by diplomats and financial markets around the world.

For example, Bolsonaro appointed Paulo Guedes, alumni of the University of Chicago, as Finance Minister. Another Chicago alumnus, economist Roberto Castello Branco, now manages Brazil’s biggest oil company Petrobras.

Former World Bank managing director Joaquim Levy was tapped to head Brazilian Development Bank BNDES and yet another University of Chicago economist, PhD Rubem Novaes, took charge of state-owned Banco do Brasil.

The new team of bureaucrats and advisors is often referred to as the “Chicago Oldies” in reference to the “Chicago Boys,” a team of Chilean economists prominent around the 1970s and 1980s, the majority of whom trained at the Department of Economics of the University of Chicago under Milton Friedman and Arnold Harberger.

Behind these key appointments emerges a clear strategy that Bolsonaro had been touting since his candidacy; he wants the state to privatize more assets to lower Brazil’s cost of governing, and that includes Brazil’s crown jewel – Petrobas, Brazil’s state oil company.

So far Bolsonar can be hopeful that all his initial actions will bear fruition soon as he has been showered with positive growth forecasts.

Brazil Economic Outlook

According to the World Economic Situation and Prospects 2019 report issue bu the UN, Brazil’s economic growth could rise to 2.1% in 2019 and 2.5% in 2020. Compared to its 1.4% growth in 2018, the forecast cultivates hope in Brazil’s early economic recovery.

According to the World Economic Situation and Prospects 2019 report issue bu the UN, Brazil’s economic growth could rise to 2.1% in 2019 and 2.5% in 2020. Compared to its 1.4% growth in 2018, the forecast cultivates hope in Brazil’s early economic recovery.

This is supported by another economic report issued by the OECD. It also projects growth acceleration for Brazil’s economy during 2019 and 2020, while low inflation, moderate wage growth, and decreasing unemployment are expected to strengthen private consumption and with that increased foreign investments.

On top of that, it is expected that stabilizing credit markets and greater policy certainty will support market recovery and future growth.

For example, Credit Suisse suggests that improving business sentiment coupled with stability in local markets and relatively low-interest rates would prompt a 9.3 percent jump in fixed investment.

Brazil Risk Assessment 2019

So far Bosonaro and his team are off to a good start. International investors, diplomats, and the global business community are all in favor of what Bosonaro has been promoting for his country. But there are clouds building on the horizon and as promising and enticing as those early successes might be, it might all turn back into gloom and doom in a moments notice. As the OECD reports, “The fragmented political landscape will make it difficult to create a political consensus for key reforms, which is desperately needed.” Political uncertainty around the implementation of reforms remains significant and could derail the recovery. Here are some of the risk factors that need to be considered.

Pension Reforms

One of the most challenging aspects to fix Brazil’s economy is pension reform, and its output will decide the fate of the country’s economic recovery. Brazil’s pension system currently allows many people to retire in their mid-50s.

The country has to hand out 3% of its GDP for the retirement fund. Unless Brazil’s economy is growing at 3%, which it hasn’t done in at least eight years, then the Brazilian government has to take out loans to pay its pensioners.

Bolsonaro at the moment is preparing a proposal to gradually increase the retirement ages to 62 years old for men and 57 years old for women. But the bill will be highly unpopular, that he cannot even count on his base in the military to support it as they have been one of the biggest beneficiaries.

Brazil investors are also doubtful that Bolsonaro can get pension reform passed in Congress. However, Bolsonaro with his authoritarian style of leadership may find it easier to pass unpleasant policies, even at the risk of losing popular support. In an interview with Washington Post, the far-right leader acknowledged that his unpopular policies might make a second term impossible.

Fiscal Health

The other major worry lays in the country’s fiscal health. Brazil lost its investment-grade rating in 2015 and its efforts to reform public spending have not been comprehensive so far. The fiscal deficit estimated at around 8% last year. Brazil’s debt-to-GDP ratio hit 78% of GDP in 2018, its highest in a generation. The IMF forecasts it to go above 80%.

The economy also lacks competitiveness. Brazil ranks 184 out of 190 countries in the World Bank’s doing business rankings on paying taxes. It takes 1,958 hours in a year in Brazil to pay taxes, according to the Forbes article, in contrast to Singapore’s 49 hours. It scrapes tax payments and collection, particularly from small businesses who may not be able to afford external services to pay taxes.

Meanwhile, for ease of doing business, the aforementioned OECD report ranks Brazil on 109 position out of 190, much lower compared to other emerging market such as China (46) and India (77). However, during World Economic Forum in Devon in January, Bolsonaro pledges to bring about economic change, saying that by the end of his term Brazil will be ‘in the ranking of the 50 best countries to do business with’.

Political Will

“The only mistake of the dictatorship was torturing, and not killing.’ Thus responded Jair Bolsanaro, new President of Brazil, to a question regarding the activities of the military junta that ruled South America’s biggest country for decades in the 20th century.

Riding a wave of anti-corruption sentiment directed at the Worker’s Party, the far-right candidate was swept to power over the rather dull opposition and has already gone to work promoting a vigorously right-wing agenda to the delight of investors around the world.

Bolsonaro is a conservative of the old school – and by old, some would argue, that means positively 19th century. He has previously stated that if he saw to men kissing he would beat them up, that torture should be legal, that tax evasion is a sound and legitimate activity, that people searching for the bones of ‘disappeared’ loved ones were ‘dogs’, that women working has caused a rise in the number of homosexuals, and that if he was president, he’d leave the UN.

He has already transferred control of indigenous lands in Brazil to the ministry of agriculture, an institution largely in the pocket of agribusiness. The move has been dubbed a ‘genocide’ by left-wing outlets, who lament the impact this will have on the delicate lifestyles of any uncontacted tribes in the Amazon.

Bolsonaro’s election is largely the result of a complete, calamitous failure of the Worker’s Party to rein in corruption.

Like many other populists, he is seen as determined, unconventional, and, above all, capable of undoing the various entrenched interests that have kept Brazil’s levels of inequality staggering and economic growth good, but not great.

His unwillingness to be PC is seen as a rejection of frivolous social posturing for the sake of meaningful reform.

In other words, a lot of what got Bolsonaro elected is what got Viktor Orban, Donald Trump, and Rodrigo Duterte elected.

It’s the investor’s individual understanding and acceptance of political risk, but in Brazil’s case, they are substantial. This should be kept in mind when we summarize our findings below.

Conclusion

At the grand event in Davos in January this year, Bolsonaro had a chance to shine and convince the world community of his visions for a better tomorrow. It was a big disappointment! In short, Jair Bolsonaro, the keynote speaker, was a huge disappointment in my eyes and indirectly a warning sign to emerging markets investors. His speech was just 16 minutes long and read from the teleprompter.

The content was boring and uninspiring. Lot’s of lip service to the investors and business community read from a script, but nothing beyond that. You just couldn’t brush off the suspicion that this man didn’t really believe in what he just read from his notes prepared by others.

Instead, the impression he made on me was, that of a stubborn, arrogant and defiant man who had better things to do than convince critics and non-believers.

Yes, under his rule we can expect widespread tax cuts, paring back of social programs, reducing benefits, deregulation, the opening of huge tracts of land for development, a realigned foreign policy, and a generally more combative tone.

But as good as Brazil’s economic outlook might be and as good as the lip-service may sound to investors there are clear warning signs for investors.

Bolsonaro needs to work fast to fulfill his election vows of improving the economy. In an interview with Forbes, Jan Dehn, Head of Research for Ashmore Group in London, a $70 billion asset manager that invests in Brazilian government bonds, said that Bolsonaro has 6 months to get something going on – otherwise, the company will “imply meaningful repricing that will weaken the Brasilian real once more.”

The appetite for Brazilian stocks from American fund managers will also depend on the direction of the dollar. If the dollar stops strengthening, foreign investors will be more interested in emerging markets in general. If it goes the other way, less money will flow into Brazil’s stock market or any other emerging market for that matter.

Emerging Markets Lesson Relearned

Back in Brazil, one of Bolsonaro’s son who is also in politics, is involved in a political scandal that reeks of Mafia structures and violence. Jair Bolsonaro own frequent political slurs on TV and social media are worrisome and anachronistic, to say the least.

Investing in emerging markets is more than just high growth outlooks and cheap valuations. The factor of country or political risks are often overlooked or neglected by investors in the West, especially at times of general optimism.

Brazil, Argentina, and many other Latin American countries have a long tradition of political scandals, coup d’etat and corruption scandals with sever economic and financial consequences for investors.

In 2019, we might get a bitter aftertaste of former lessons learned as a new generation of investors are relearning the old lessons of emerging markets investing. A long forgotten risk factor is making its comeback where most emerging markets experts still dream of growth and value – political risk.

Often talked about but many times neglected, emerging markets risk factors are unique and challenging. Yet, they determine investment performance. Brazil could lead such a new wave of old lessons relearned with very disappointing performance for over-eager investors.

Appendix

References

https://www.oecd.org/eco/outlook/economic-forecast-summary-brazil-oecd-economic-outlook.pdf

https://www2.deloitte.com/insights/us/en/economy/americas/brazil-economic-outlook.html

https://www.bbvaresearch.com/en/publicaciones/brazil-the-economy-will-grow-2-2-in-and-18-in-2020/

https://www.aei.org/publication/bolsonaro-in-davos-a-missed-opportunity/

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/769112/Brazil_1018.pdf

https://www.cia.gov/library/publications/the-world-factbook/geos/br.html